STUDENT TALK The Holy Trinity: Banking, Budgeting, and Saving

According to Bankrate, about 5.4% (or 7.1 million) American households are unbanked, and 17% were underbanked in 2019. The unbanked are typically people who don’t rely on financial institutions to help them manage their finances. They never interact with financial institution branches in any way, shape, or form. The underbanked, on the other hand, may have a checking or savings account but otherwise don’t interact with their financial institution. They rely on retailers to wire funds or purchase money orders, and opt to save money in a container at home. In both cases, payday lending can be a very real, and very dangerous financial path taken when funds are needed. This can put people who aren't as aware of the benefits of a formal financial institution or aren't comfortable with financial institutions in a very precarious position.

There could be a variety of reasons people are unbanked or underbanked. Some feel they won't be accepted due to bad credit history or they may be concerned they'll be taken advantage of with fees and unexpected costs. Still others have a general lack of trust in our financial system. or may be new to banking in the U.S. and not understand why a bank or credit union would be a better choice than keeping money in a jar at home. This post is written to address some of those concerns and provide tips on how banking can factor into budgeting, saving, and making a financial choice that will improve your financial life.

The First Arm - Banking

Choosing a Financial Institution

What's the difference between banks and credit unions?

The main difference between the two revolves around the fact that banks are for-profit institutions and credit unions are not-for-profit. While some smaller community banks get involved in their community, and big banks have deep pockets and are known to contribute to large organizations, credit unions place an emphasis on serving their immediate community members. That's been a part of credit unions from the start. It's why the general credit union motto is, "People Helping People." It's what they believe and exemplify.

How do I make a decision - bank vs. credit union?

The best way is to ask yourself the following, "What am I looking for in a financial institution?"

- Do you have funds you can leave in savings and want to earn money on them?

- Do you want to have ATM access country-wide no matter where an institution's branches are?

- Do you want customer service that is friendly and knowledgeable?

Having these answers handy as you do your research will help. But doing the research is the important part. Start with a list of possible options, banks, and credit unions near your home, work, or school. Narrow it down according to your criteria. (If rates are part of that criteria, Bankrate is a great site for comparing rates.)

Concerned about the safety of your money? With a regular financial institution, you won't need to be. The FDIC (Federal Deposit Insurance Corporation) and NCUA (National Credit Union Association) are federal entities that work to protect your money in banks and credit unions, respectively. Most financial institutions are insured. Keeping your money in a jar at home? That's definitely not insured! But if you're intending to deposit a large sum of money, in excess of $250K, you might want to do more research and speak to the institutions about your funds and the insurance they carry. In some cases, depositing money in more than one institution may be needed to protect larger sums.

Don't let the presence of a local branch (or the lack of a local branch) stop you from choosing a specific financial institution. Mobile and online banking are options that are constantly evolving. In fact, mobile and online banking are becoming more and more the option-of-choice nowadays. There are even financial institutions that are solely mobile/online. These "online-only" entities sometimes offer better rates and lower fees since they don't maintain brick and mortar locations, but you're also not going to get personal service and someone you can meet with to discuss issues or questions. When I started out in college, I personally chose an online bank for my savings account because they had an amazing interest rate before the pandemic. Now that the world has changed and my knowledge of both online banking AND virtual banking has expanded, I understand that rate isn't all there is to banking, and in fact, many credit unions can compete with the best of the online banks and provide more community-focused, personal service. Let's face it, rates and needs change. You may open an account online then your life changes and it's time to make another choice. With banks, and credit unions, online or not, stay in touch with what's being offered. You may find yourself considering a change. It never hurts to check out the competition and think back on your needs and how your bank or credit union or online provider supported you when you needed them most.

What do I need to know before opening a bank or credit union account?

The first thing to keep in mind is, "Don’t be swayed by special offers at account opening unless they will have true value to you." Getting a small amount of cash to open an account with a financial institution, when it doesn’t offer the services you want, is not a good idea. An offer of a discounted loan rate or the option to skip a loan payment or two, when you're in the market for a loan? That may represent enough value to make it worth your business.

Opening a financial account involves paperwork. Be sure to read through the disclosures, either at opening or soon thereafter. You'll want to be aware of the fees (e.g., closing, maintenance, overdraft) and any balance requirements associated with the account before you open it. Ask about these items as part of your initial research and make notes so you can refer back when you're making a final decision.

At a Bank you're a customer, at a Credit Union you're a member

What's with this whole "membership" thing at credit unions? That's the community part of the cooperative way to bank. When you open an account with a credit union, they consider it "joining" the credit union. You actually become a partial owner of the cooperative that is the credit union. Credit unions are collaborative community-based entities. Of course in the grand scheme, it may seem a very small difference, but credit unions do not take that "small difference" lightly. Decisions on management and operation are made with the specific credit union members’ best interests in mind. The credit union will often ask members for feedback or offer opportunities to contribute in focus groups and surveys to assist the credit union’s planning and strategy. If you're looking for a financial institution where your opinion matters, a credit union is a good choice.

Financial institutions will usually require you to make an initial deposit to start the account opening process. They will also want to confirm your identity before opening an account. In fact, they are required to ask for certain information to determine both who you are, and who/how the funds in your account will be owned and used. This is part of the USA Patriot Act and the AML Act, set up to prevent money laundering and illegal use of funds. I mention this last step as a reminder for international students in particular. If you are an international student, it's important to have the appropriate documentation needed when you are looking to open an account. MIT FCU offers membership to international students and has members from all around the world. They’re also accustomed to dealing with issues like international wires, providing 24/7 support, and understanding the confusion that can come up for members who are not US citizens and unfamiliar with banking in the US.

The Second and Third Arm of the Holy Trinity - Budgeting and Saving

Budgeting - That thing we should all do, but some do it with a bit more ease

Ahh, budgeting, one of the things you know you should do, but where to start? Budgeting is setting a financial goal and steps to achieve that goal. Whether that be saving X amount of your paycheck this month or cutting back on your "boba spending" per week to help you on the way to get to the desired end goal. Budgeting can also involve setting up expense categories for your needs and wants, to ensure you allocate your money to address immediate needs, such as food and rent but also having something set aside for future goals and living your life today. because let's be honest if you can't enjoy life sometimes who wants a budget? But how do you do it?

I’ve tried both meticulously tracking purchases on a spreadsheet, and simply setting a ballpark budget per month taking into account what I need for "must-haves" and then allotting myself an amount to spend. In the former case, I usually got so overwhelmed with remembering to track every purchase that I abandoned the effort halfway through the month. While I haven’t had to monitor my spending too much since getting stuck in quarantine at home, I’ve found the latter method, setting a ballpark budget per month, to be more in line with my lifestyle. I’m typically not a big splurger, so just making sure I spend below my set monthly budget is enough to make sure I don’t squander my savings.

Ultimately, I think that’s the key to budgeting: finding a method that fits your lifestyle. If you’re someone who likes to micromanage and crunch numbers, then go with the spreadsheet method or find a budgeting app that lets you be more hands-on with how you track your spending. If you prefer the opposite, there are also budgeting apps that keep track of your spending for you and issue warnings when you’re spending too much or reaching limits you've set for yourself. Financial institutions may also offer calculators and other money management tools through online banking or mobile apps to give you a comprehensive view of your finances. MIT Federal Credit Union offers its Money Management Tool, which is a hybrid of both approaches, for free in their online banking platform.

Saving even when it seems there's nothing left

Coming from a low-income background, I was always worried about how I’d find the money to save for post-grad life. I never landed a lucrative internship. The money from my few short-lived UROPs went towards summer rent and other living expenses. Fortunately, I am on full financial aid and get a refund for the money I don’t spend on meal plans and MIT’s extended insurance plan. I spend the refund on living expenses, rather than savings, but I do save what’s leftover at the end of each semester.

Saving is essential for a variety of reasons. The two most important are to establish an emergency fund and to make sure you have enough money to live comfortably into retirement. Perhaps an emergency fund doesn't take too long to save for, but that retirement piece, that's a lifelong project. In general, experts recommend you save 15% of your salary and start as early as possible. Also, if your employer offers a matching benefit for a 401K, take full advantage. Otherwise, it’s leaving money on the table. In fact, while 15% may seem like a lot, if you consider that part of that 15% is the matching funds, you're already on your way!

Even if you can only afford $100 a month or less for a retirement fund, get started now. Getting it set up in your twenties, as soon as you have an income, sets you on the right path. Start small with a certificate of deposit or an IRA Savings account. If an employer offers a way to have funds directly withdrawn from your paycheck, do it and set up an automatic increase each year, say 1%. You’ll never see the money, learn to function without it, and, assuming you receive a raise each year, that 1% increase won't even be felt, except by your retirement fund.

Unfortunately, the whole idea of saving assumes a lot of things:

- you can afford to put any part of your paycheck into savings

- you have a savings account

- and/or you have a steady income.

It’s a privileged practice that not everyone can take part in. But if you can, don't delay. You'll enjoy the rewards in the future. If you can't, set it as a goal. Try cutting certain basic purchases from your weekly spend, like coffee, boba, uber eats, or any other little thing you could either do without or do differently to reduce the cost. Then set those funds aside or deposit them into an account. It's a start. Anything is better than nothing.

Following italicized notes are from MIT Federal Credit Union: As mentioned, this post was written as part of a PKG Social Impact Internship. PKG's mission is: The PKG Center taps and expands MIT students’ unique skills and interests to prepare them to explore and address complex social and environmental challenges. We educate students to collaborate ethically and effectively with community partners to engage in meaningful public service, today and in their lives beyond MIT.

Towards that end, additional information below from our blogger talks about the inequity some members of marginalized communities may experience when it comes to savings opportunities and the racial wealth gap. At MIT Federal Credit Union we do offer assistance and tools for budgeting, educational sessions on credit, budgeting, and other finance-related topics. These financial education opportunities are open to the public, regardless of membership, and are free of charge. If you are struggling to save or have concerns about banking with a credit union, please contact us for more information.

There is inequity in savings opportunities.

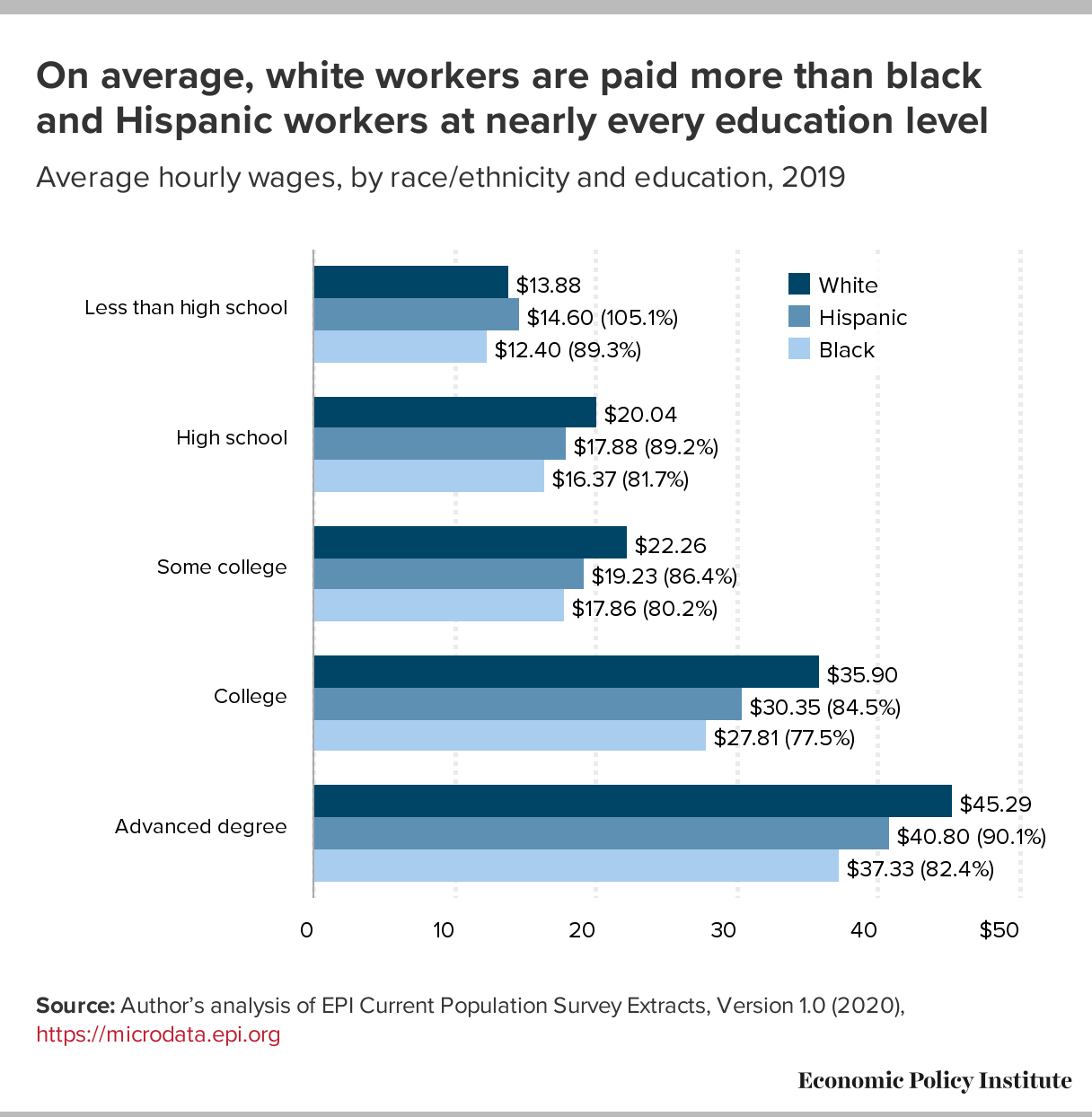

According to Forbes, 21% of Americans aren’t saving, and 75% of Americans that are saving don’t save enough for retirement. On top of that, White workers are consistently paid more than Black and Hispanic workers across nearly every educational level. This racial wealth gap stems from the institutionalized racism that has systematically allowed women, people of color and other marginalized groups to be discriminated against by their employers. If you're saving from what you earn, that gap also impacts those marginalized groups' ability to save for and live a comfortable presence in retirement.

While saving money is a good financial practice to learn, we should acknowledge that it is a practice many people struggle to do for various reasons. There should be no guilt attached to someone's inability or lack of funds to start a savings plan. Considering the disparities the coronavirus pandemic has exposed and exacerbated, I want to encourage those who can, to support local minority-owned businesses and to advocate for our less privileged peers. And if you are among those who haven't yet started to save, give it some consideration. Whether you start today, or when things take a new direction for you, it is never too late, or too early to get started.

Keep the ideas addressed in this post in mind. Start establishing your finances by opening an account with a bank or credit union. Budget to make sure you’re not spending beyond your means. Save so that you have the money to spend on things that bring you joy, invest in the communities you care about, and support yourself through retirement.

Sites used for research:

« Return to "Money Talk Blog"

- Share on Facebook: STUDENT TALK The Holy Trinity: Banking, Budgeting, and Saving

- Share on Twitter: STUDENT TALK The Holy Trinity: Banking, Budgeting, and Saving

- Share on LinkedIn: STUDENT TALK The Holy Trinity: Banking, Budgeting, and Saving

- Share on Pinterest: STUDENT TALK The Holy Trinity: Banking, Budgeting, and Saving